|

||

|

Name

Cash Bids

Market Data

News

Ag Commentary

Weather

Resources

|

Are Wall Street Analysts Predicting Weyerhaeuser Stock Will Climb or Sink?

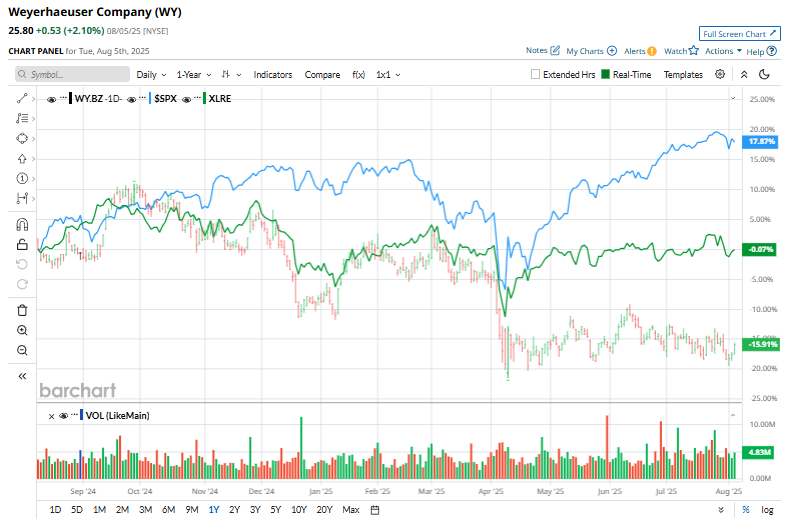

Valued at a market cap of $18.2 billion, Weyerhaeuser Company (WY) is one of the largest private owners of timberlands in the world, managing over 10 million acres of forests in the U.S. and with long-term licenses in Canada. Headquartered in Seattle, Washington, WY operates as a real estate investment trust (REIT) and is a key player in sustainable forestry, wood products manufacturing, and land development. Shares of WY have underperformed the broader market over the past 52 weeks. WY has declined 17.1% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 21.5%. Shares of WY are down 8.4% on a YTD basis, compared to $SPX’s 7.1% rise. Zooming in further, WY has also trailed the Real Estate Select Sector SPDR Fund’s (XLRE) 2.8% gain over the past 52 weeks and 2.7% rise in 2025.

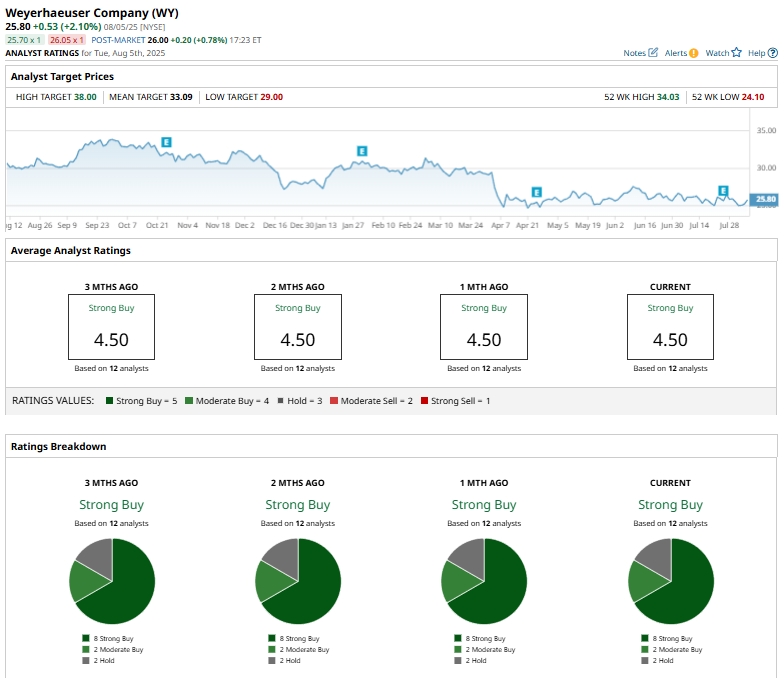

On July 24, WY shares dipped 1.1% after the company announced its fiscal 2025 second-quarter earnings. Despite macroeconomic uncertainties, the company achieved solid performance in real estate and climate-related initiatives, posting $1.9 billion in net sales and $0.12 per share in EPS. It remained committed to returning capital to shareholders, completing a $100 million buyback and launching a new $1 billion authorization, while expanding its strategic forest holdings in the Southeast. For the current fiscal year, ending in December 2025, analysts expect WY’s EPS to decline 41.5% year-over-year to $0.31. However, the company’s earnings surprise history is solid. It beat or met the consensus estimates in each of the last four quarters. Among the 12 analysts covering the stock, the consensus rating is a “Strong Buy.” That’s based on eight “Strong Buy” ratings, two “Moderate Buys,” and two “Holds.”

On Jul. 28, Truist Securities reiterated its "Hold" rating on Weyerhaeuser but lowered the price target from $30 to $29. The mean price target of $33.09 represents a premium of 28.3% from the prevailing price levels. The Street-high price target of $38 implies a potential upside of 47.3% from the current price. On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here. |

|

|